They want to push everyone over to online services. Don’t be surprised if they announce that they will be discontinuing desktop in a few years. They are currently pushing all of their energy into getting all of the kinks out and features added into QBO. My former accounting manager had a liaison at Intuit that spilled all of this to her. Federal and state payroll taxes are calculated, filed and paid automatically in all three plan tiers. Local filing is included in the Premium and Elite plans.

Launch of ‘QuickBooks Online Advanced’ aims to empower accountants and accelerate small business growth – Yahoo Finance

Launch of ‘QuickBooks Online Advanced’ aims to empower accountants and accelerate small business growth.

Her experience ranges among small, mid-sized, and large businesses in industries like banking and marketing to manufacturing and nonprofit. We considered user reviews, including those of our competitors, based on a 5-star scale; any option with an average of 4+ stars is ideal. Also, any software with 1,000+ reviews on any third-party site is preferred. Gusto, Paychex, Rippling, and Patriot earned a perfect rating in this criterion. In this criterion, we assess whether the software’s ease of use, pricing, and the width and depth of its payroll and HR tools are ideal for SMBs.

Uninstall and reinstall QuickBooks

Are you offering benefits like health insurance? You will need to have your paperwork and information handy before you start completing this section. Go up to thePayrollheading in the upper left and click onPay Schedules.

OnPay’s key feature is its ability to allow for unlimited pay runs. This allows businesses to run payrolls in accordance to their preference without having to pay additional fees. This may come in the form of corrections and pay run cancellations. Data entry is also eliminated using the system, with employee data saved in a secure vault. The interface is user-friendly and designed for mobility, allowing users to quickly and easily process payrolls.

Rippling for Accountants Pricing

The Pay History icon opens a list of previous payrolls. You can drill down on these dates to see underlying detail. In addition, you can see and edit very abbreviated employee records—just contact and basic pay information. Payroll service and software should be simple to set up, be customizable, and have a user-friendly interface. We also looked at whether the provider offers live support and integration options with online tools that most SMBs use.

SurePayroll’s partner accountant program also includes free account setup and free access to its payroll tool that you can use for your firm—provided you have 10 or more clients. New hire reporting, an HR library with business forms, and a labor compliance kit with e-posters for federal and state updates are some HR tools you can get with Paychex Flex.

Employee Records

Once the user creates e-payment or prepares returns, the user attains compliance report without any extra charges. With the use of the Enhanced Payroll tool, reporting and monitoring task such as exporting reports to tax liabilities and period comparison has become easier. The hassle of printing or emailing checks is removed with the QuickBooks Direct Deposit feature provided by QuickBooks Enhanced Payroll for accountants. If you cancel your service, we will provide historical access to your data for 7 years. QuickBooks Online Payroll is a modern experience with more features, more automation, more time savings, and better ongoing development support.

Patriot Payroll, which is the least expensive option in this guide, lets you handle client payroll efficiently. It also comes with time tracking and basic HR solutions for monitoring staff work hours, creating overtime rules, and managing https://quickbooks-payroll.org/ an online employee database. While these tools are paid add-ons, adding both to Patriot’s payroll platform makes it ideal for your clients who employ mostly hourly workers and want to accurately capture employee attendance.

Tracking capabilities ensure that you are on top of your processes. Sage 50cloud is an online accounting solution for small and medium-sized businesses that offers features such as taxes, inventory, budgeting, cash flow, and invoicing. It provides a wide range of add-ons for credit card processing, payroll, and more. Organizations can utilize the app’s built-in accounting best practices to qb online payroll for accountants stay compliant and to track their finances. You can make payments on-the-go and bill customers, and provide your accountants real-time access to accounting books. It supports financial reporting, online payment, multi-currency, business performance dashboard, sales tax calculation, and more. The best payroll software for payroll service providers and accountants is Quickbooks Payroll.

In case you feel these tools aren’t enough, the platform has open API capabilities and native integrations with over 500 third-party applications so you can extend its functions as needed. For clients only requiring payroll and automated tax filing solutions, Patriot Payroll is a great choice as it is affordably priced and has full-payroll services.

List of Few Common Payroll Errors in QuickBooks

Some competitors like Gusto also offer specialized banking options. OnPay, for example, includes a company directory and conversation feature, as well as company files and forms. Accounting firms that join Patriot Payroll’s partner program enjoy discounted rates based on the number of clients they have. It offers product discounts of up to 20% for its payroll, accounting, time and attendance, and basic HR modules.

The vendor has elected to place the software on a by-quote basis due to its modular nature.

For health plans available across the US, consider any of the other providers on this list .

Setting Up QuickBooks Payroll reduces the effort of remembering the payday.

It also offers new hire onboarding, background checks, learning management, access to HR experts, and an online employee handbook—provided you sign up for one of its higher tiers.

Starting 2020, QuickBooks came up with the QB enhanced payroll for accountants.

QuickBooks Payroll offers three plan levels, but what sets QuickBooks Online Payroll apart from other payroll providers is that even the lowest priced payroll plan offers full-service payroll processing.

Prior to becoming a writer, she worked as an HR specialist at several multinational companies. Charlette has over 10 years of experience in accounting and finance and 2 years of partnering with HR leaders on freelance projects. She uses this extensive experience to answer your questions about payroll. The Ascent is a Motley Fool service that rates and reviews essential products for your everyday money matters. We’re firm believers in the Golden Rule, which is why editorial opinions are ours alone and have not been previously reviewed, approved, or endorsed by included advertisers. The Ascent does not cover all offers on the market.

Why trust QuickBooks for payroll?

Set up your payroll once, and never worry about it again. All your salaried employees whether full-time or part-time will get paid automatically every time. The software is free for use, providing a great value for small business, startups, or even individual HR managers looking for an optimal HR service solution.

Let’s explore the way inventory moves through a business financially. A second journal entry reduces the account Inventory and increases the account Cost of Goods Sold. There is no way to tell from the general ledger accounts the cost of the current inventory or the cost of goods sold.

Cost of goods sold is an accumulation of the direct costs that go into the goods sold by your company. This includes the cost of any materials used in production as well as the cost of labor needed to produce the goods. It doesn’t include indirect expenses such as distribution costs and marketing costs. Calculating and tracking your cost of goods sold is one of the most important tasks of a bookkeeper in order to make sure your business is profitable. Note https://business-accounting.net/ that the reported costs on the financial statements ($260 for ending inventory and $1,820 for cost of goods sold) are identical under both perpetual and periodic systems. However, as will be demonstrated in the next chapter, this agreement does not always exist when inventory items are acquired during the year at differing costs. The inventory in this journal entry is the amount that is remained from the opening inventory deducting the ending inventory.

Additional Costs and Landed Costs

By the time shipment takes place, the accounting period covering the invoice date is locked. If the user attempts to authorise the shipment with default date 28th of November, they will receive an error. User will have to enter a new shipment date after the locked date in order to authorise the ship tab.

What is cost of goods sold in income statement?

Cost of goods sold (COGS) on an income statement represents the expenses a company has paid to manufacture, source, and ship a product or service to the end customer.

This is because we only update the inventory balance periodically which is usually by physically counting the actual inventory at the end of the year. Likewise, we can make the journal entry for the cost of goods sold and the reduction of the inventory by debiting the cost of goods sold account and crediting the inventory account. This is because, under the perpetual inventory system, we need to update the balance of inventory on the balance sheet every time there is an increase or decrease of the inventory. The LIFO method will have the opposite effect as FIFO during times of inflation. Items made last cost more than the first items made, because inflation causes prices to increase over time.

Select Subperiod Ending

The cost incurred in purchasing goods or services to sell them and generate revenue is called as the cost of goods sold. The account that is used track this cost is named as the Cost of Goods Sold account. There can be changes in the Cost Of Goods Sold throughout the accounting period. When creating a COGS journal entry, increase expenses with a debit, and decrease them with a credit. Your COGS can likewise determine if you’re spending a lot on production costs.

The second journal entry debits the Material and Labor accounts and credits the Inventory Change account. Previously, only one journal entry was generated for the COGS split.

How to Record a Cost of Goods Sold Journal Entry 101

Cost of goods sold documents the inventory and purchase amounts spent on products or services produced, manufactured, or sold during a given time period. COGS can be calculated journal entry cost of goods sold per item by multiplying the cost per unit by the number of units sold. To record a cost of goods sold journal entry, COGS is debited and the inventory account is credited.

Calculating and tracking COGS throughout the year can help you determine your net income, expenses, and inventory. And when tax season rolls around, having accurate records of COGS can help you and your accountant file your taxes properly. Determining the cost of goods sold is only one portion of your business’s operations.

Cost of Goods Sold Journal Entry

It is time consuming and costly for companies to physically count the items in inventory, determine their unit costs, and calculate the total cost in inventory. There may also be times when it is necessary to determine the cost of inventory that was destroyed by fire or stolen. To meet these problems, accountants often use the gross profit method for estimating the cost of a company’s ending inventory. Journal entry for goods sold will increase both the total assets on the balance sheet and total revenues on the income statement regardless of the goods sold are made for cash or on credit.

Instead, the average price of stocked items, regardless of purchase date, is used to value sold items.

For most companies, the Specific Identification method is far too costly and the additional information that could be gained is of little value.

For example, the COGS for a baker would be the cost of ingredients, and labor if she has an assistant who helps produce items for sale.

After calculating your cost of sales for the period, you can now proceed to find your business’s gross profit for the same period under review.

Without sales the company’s cash remains in inventory and unavailable to pay the company’s expenses such as wages, salaries, rent, advertising, etc.

Free Financial Modeling Guide A Complete Guide to Financial Modeling This resource is designed to be the best free guide to financial modeling!

You should record the cost of goods sold as a business expense on your income statement.

In this example, a physical inventory count will be taken by the employees of Rider Inc. on or near the last day of the year so that financial statements can be produced. Because eight bicycles (Model XY-7) were available during the year but seven have now been sold, one unit—costing $260—remains .

So, if you want to calculate a semi-monthly daily rate, divide your employee’s annual salary by 260. A semi-monthly pay period results in 24 paychecks in a year. Because the payroll is processed fewer times for semimonthly frequencies than biweekly, employees’ paychecks will be greater. Biweekly paychecks will be be for less money, but employees will receive the two additional paychecks to make up the difference. These exceptions are adjusted on the following paycheck, resulting in a two-week lag for exceptions. In the U.S., salaried employees are also often known as exempt employees, according to the Fair Labor Standards Act . This means that they are exempt from minimum wage, overtime regulations, and certain rights and protections that are normally only granted to non-exempt employees.

The semi-monthly base salary represents 86.67 hours of pay.

To use the percent of pay period method, start by writing down the employee’s annual salary before taxes.

Examples include sexual harassment, drug or alcohol violations, or breaking state and federal laws.

Add the overtime from each of the working weeks in the semi-monthly pay period.

Moreover, calculating the salary for hourly biweekly employees is the easiest payroll process.

Salaried employees are typically paid for 260 days in a year .

Payments to hourly employees are based on the number of hours worked during a specific payroll period.

When you use semi-monthly pay periods, each pay cycle has a different number of workdays. Instead of using steps one and two, divide your employee’s new annual salary by 260 to find their daily rate. When you leave or stop working, you receive pay one or two weeks after your last day worked because of the lag from your last pay period. This lag affects most employees and is the reason why it appears that your pay was held when you started working. If you receive an annual salary and are paid biweekly, your pay reflects regular pay for a two-week period up to and including the Saturday before pay day. Exceptions, including premium pay for overtime, shift differentials, or work on holidays, are on a two-week lag.

Multiply Hourly (or Daily) Rate by Time Missed

In particular, you can use unpaid disciplinary action for full-time employees that violate your code of conduct. Examples include sexual harassment, drug or alcohol violations, or breaking state and federal laws. If you are searching for the Can you pay hourly employees semi monthly in illinois then must check out reference guide below. Substitute paraprofessionals are paid on a positive basis for each day worked. For example, the pay you receive on June 16 covers the period May 16 through May 31. Per Diem service refers to licensed pedagogic personnel serving on a day-to-day basis in a school and/or any of its programs. Employees serving on a Per Diem basis are commonly referred to as substitute teachers.

For example, you may pay your employees on the 1st and the 15th irrespective of the month’s length.

Payment is generated on a Thursday, 16 days after the pay period end date.

Unlike a bi-weekly payroll, which has 26 payments in a year, a semi-monthly pay schedule has only 24 pay periods.

For most cases, such as unpaid PTO or an employee that started in the middle of a billing cycle, the daily wage will suffice.

Education—The higher the attained level of education of a person, the higher their salary tends to be.

Most salaries and wages are paid periodically, typically monthly, semi-monthly, bi-weekly, weekly, etc.

Monthly pay periods require businesses to process payroll only 12 times per year, compared to 52 times a year for those https://online-accounting.net/ running weekly payrolls. However, for most employees, it is difficult to wait an entire month for a paycheck.

Calculating semi-monthly salary changes?

Traditionally in the U.S., vacation days were distinctly separate from holidays, sick leaves, and personal days. Today, it is more common to have them all integrated together into a system called paid time off . PTO provides a pool of days that an employee can use for personal leave, sick leave, or vacation days. Most importantly, the reasons for taking time off do not have to be distinguished. There’s no need to fumble over whether to designate an absence as sick or personal leave, or to have to ask the manager to use a vacation day as a sick day. There are, however, some downsides to having them combined. Some employees may choose to pay hourly semi-monthly employees for 86.67 hours, and then make adjustments on the next pay period.

That time varies among employers and can be negotiated upfront.

Unlike salaried employees, hourly workers, who are typically classified as non-exempt employees, are eligible for overtime and therefore do not qualify for prorated salaries.

Gender—Men earned an average salary of $55,432, and women earned $44,564.

An employer needs to pro rate salary for an employee mid pay period.

Run for someone who works only part of their normal pay period, e.g., a new hire or terminated employee.

For instance, if they only worked 14 days in a month consisting of 22 work days, you’d divide 14 by 22. After that, multiply the result by their normal monthly pay. For example, if their normal pay is 4,000 dollars, you’d divide 14 by 22 to get 0.64. Finally, deduct any withheld taxes and retirement funds, as you would for their regular paycheck. If a salaried employee was on duty for only one day of the month he should be paid for the entire month. If the employee receives a raise as a an exempt employee a wise employer would start the raise effective the beginning of the month .

Can you pay employees monthly in Illinois?

You may need to specify that the pay period ends earlier for semi-monthly payments than biweekly payments. You may even want to issue your employees a payment calendar so that they understand which pay period their paycheck is covering. Monthly A monthly payment frequency results in 12 total paychecks per year. Dividing the total yearly salary by 12 will give you the gross pay for each month. Usually, a monthly payment frequency is used for salary employees, but hourly employees can be paid monthly as well. Carole’s pay is this daily rate times the number of days worked.5 times $253.85 is $1,269.25.So why is it a best practice to minimize variances between the length of semi-monthly pay periods? The easiest way to explain this is to compare Carole’s pay for the period November 9 through 15, with the pay owing, if she had been hired effective November 24.

How much is 50k semi monthly?

$50,000/18 pay periods = $2,777.78, is your gross semi-monthly pay. A 12 month employee salary is calculated as follows: $50,000/24 pay periods = $2,083.33 , is your gross semi-monthly pay.

The day rate is then multiplied by the actual number of days worked. However, in the 1st semi-monthly pay period in November, 2015, there are 10 Monday-to-Friday work days. In the 2nd semi-monthly pay periods in that month there are 11. Her annual salary is $66,000 and is paid on a semi-monthly basis. Her regular hours of work are 37.5 hours/week, Monday to Friday.

Adjusting Your Payroll for a Prorated Salary

Men aged 45 to 54 had the highest annual earnings at $64,740, and women earned the most between the ages of 35 and 44 at how to prorate salary for semi monthly $48,984. However, states may have their own minimum wage rates that override the federal rate, as long as it is higher.

In general, accountants must foot many different columns of data in order to find a total for a particular period of time or of a certain piece of information. footing in accounting It is also important when verifying that data or information is correct. Let’s say the T-account listed below shows the inventory transactions for Macy’s (M).

Table of Contents

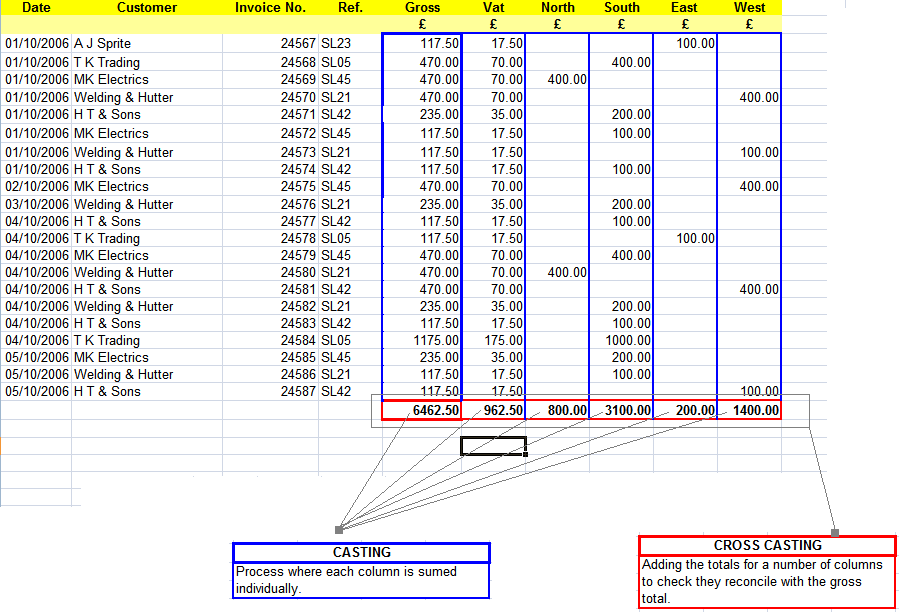

Footing means getting the sum of the amounts entered in the debit and credit columns of an account. In the following table crossfooting means adding 121 + 176 + 66 to be certain that its total of 363 is equal to the total or sum of the “Total” column’s 363. In sales analysis, footings can be used to calculate and compare the total sales for different products, regions, or time periods. By totaling the sales figures, footings enable decision-makers to identify the highest-selling products, identify growth opportunities, and analyze sales trends.

Types of Footings

This visual representation made it easier for accountants to quickly reference and comprehend the totals. While the advent of modern accounting software has made footings less apparent in physical documents, the concept still holds immense significance in the digital age. Footing information simply means to add together all of the data in a particular column.

Definition of Crossfoot or Crossfooting

This information can then inform marketing strategies, inventory management, and resource allocation. These are just a few examples of the types of footings employed in accounting. The choice of footing depends on the specific purpose of the analysis, the structure of the financial data, and the desired level of detail and comparison. The term “footing” originated from the practice of writing the final sum at the foot or bottom of a column.

Footings: What it Means, How it Works, Example

When you foot the columns on one side, the sum must match the foots on the other. If there is no match, then the columns “don’t foot,” meaning either the math or one or more of the entries are in error. To cross foot means to verify, or cross verify, that the sum of the totals in several columns agrees to a grand total. Footnotes to the financial statements serve as a way for a company to provide additional explanations for various portions of their financial statements. Footnotes to the financial statements thus report the details and additional information that is left out of the main financial statements such as the balance sheet, income statement, and cash flow statement.

What does crossfoot mean?

Assume the following amounts were entered in the service equipment account during the period.

Each of the five rows reports one product and each of the 12 columns reports one month.

For example, descriptions of upcoming new product releases may be included, as well as issues about a potential product recall.

Account balances are the amounts that are reported in the financial statements.

While the advent of modern accounting software has made footings less apparent in physical documents, the concept still holds immense significance in the digital age.

This allows stakeholders to assess profitability and make informed decisions based on the aggregated data.

If you have a table of values, with both columns and rows, you can cross-foot to double-check your numbers. This means adding together all the column foots, and then comparing the result with the sum of all the rows in the table. You don’t need to foot a column if there is only one entry in the column.

Clear can also help you in getting your business registered for Goods & Services Tax Law. Christine Aldridge is a financial planner who has been writing articles related to personal finance since 2011. She has bachelor’s degrees in political science from North Carolina State University and in accounting from University of Phoenix.

The net amount is reported on the company’s financial statements for the period. Spreadsheets lay out numbers in rows and columns, each of which can be totaled. Imagine a sheet showing monthly sales revenue for five products over the course of a year. Each of the five rows reports one product and each of the 12 columns reports one month.

In accounting, a footing is the final balance when adding all the debits and credits. Debits are tallied, followed by credits, and the two are netted to compute the account balance. Footings are commonly used in accounting to determine final balances to be put on financial statements.

Often, these will refer to large-scale events, both positive and negative. For example, descriptions of upcoming new product releases may be included, as well as issues about a potential product recall. Often, the footnotes will be used to explain how a particular value was assessed on a specific line item.

It encompasses unique accounting practices, standards, and regulations tailored to address the distinct characteristics and requirements of each industry. Through industry accounting, businesses can provide stakeholders with accurate and meaningful financial information that reflects the economic reality of their specific industry. For example, in industries such as healthcare or construction, there are specific accounting principles and practices related to revenue recognition, project costing, and regulatory compliance. Accountants in these industries must be well-versed in these specialized accounting standards to ensure accurate financial reporting. In the world of industry accounting, accountants and financial professionals are required to possess a deep understanding of the specific industry in which they operate.

If the entries aren’t balanced, the accountant knows there must be a mistake somewhere in the general ledger.

The results of all financial transactions that occur during an accounting period are summarized in the balance sheet, income statement, and cash flow statement.

Many employers also require accounting candidates to have professional certifications, such as the Certified Public Accountant (CPA) designation.

As long as you have a solid tech stack so you can operate and collaborate efficiently internally and with clients, there’s no need to go back to pre-COVID work habits.

The first step to becoming an accounting information systems professional is to earn a bachelor’s degree.

Who sets accounting standards?

They apply their expertise and understanding of the industry to ensure accurate financial reporting, compliance with industry regulations, and effective communication with stakeholders. As industries continue to evolve, industry accounting will remain integral to capturing and communicating financial information that accurately reflects the nuances and complexities of different sectors. Industry accounting professionals must stay up-to-date with these industry-specific accounting standards and ensure compliance in their financial reporting. They play a crucial role in applying these standards to capture and communicate industry-specific financial information accurately.

An accountant using the double-entry method records a debit to accounts receivables, which flows through to the balance sheet, and a credit to sales revenue, which flows through to the income statement. Accounting is a back-office function where employees may not directly interface with customers, product developers, or manufacturing. However, accounting plays a key role in the strategic planning, growth, and compliance requirements of a company. The reports generated by various streams of accounting, such as cost accounting and managerial accounting, are invaluable in helping management make zoho books review informed business decisions. By getting ahead of trends, and focusing on the right skills, firms can use the changing accounting environment to perfect their craft and find (and retain) clients.

Soft skills will increase in importance (while technology handles transactions)

Industry accountants face challenges such as navigating complex regulations, incorporating emerging industry trends, and ensuring accurate data integration. Overcoming these challenges in industry accounting requires continuous learning, adaptability, and staying abreast of changes within the industry. It also emphasizes the importance of interdisciplinary collaboration and a deep understanding of industry-specific regulations and practices. Industry accountants must navigate these challenges to provide accurate and meaningful financial information that reflects the unique nature of businesses within their respective industries. These are just a few examples of industries with specific accounting standards.

Nowadays, digital documents and eSignatures can meet the needs of most businesses. Other examples include working with environmental consultancies like Rye Strategy to help calculate and offset a business’ emissions. For example, UK-based firm, Linford Grey has designed theirs to maximize efficiency so that the team is afforded a harmonious work life balance, no matter where they’re based. If you and your team are spending too much time performing manual tasks, reassess your tech stack. And if you have a problem that no tool can seem to solve, why not see if you can solve it yourself?

Young people want career growth and development

Throughout this article, we have explored the definition of industry accounting, discussed its importance, highlighted key concepts, and delved into its role in financial reporting. We have also explored the challenges faced by industry accountants and discussed industry-specific accounting standards and practices. From healthcare to manufacturing, technology to real estate, each industry requires tailored accounting practices to accurately capture its unique financial operations. Whether it’s the healthcare, manufacturing, technology, or retail sector, each industry has its own unique set of accounting practices and challenges. Industry accounting professionals are trained to navigate these complexities and tailor financial reporting to meet industry-specific needs.

The future of the accounting industry: 7 important trends in 2024

In addition, management accountants may also be involved in planning and budgeting, risk management, decision analysis, and performance measurement. If you’re interested in finance and accumulated depreciation want to delve deeper into the intricate financial workings of different industries, then industry accounting is a fascinating field to explore. Industry accounting refers to the specialized accounting practices and principles that are unique to specific sectors or industries. Deloitte refers to one or more of Deloitte Touche Tohmatsu Limited, a UK private company limited by guarantee (“DTTL”), its network of member firms, and their related entities. DTTL and each of its member firms are legally separate and independent entities. DTTL (also referred to as “Deloitte Global”) does not provide services to clients.

Public accounting firms typically offer opportunities for promotion and pay increases. With hard work and dedication, you can move up quickly in your career and increase your earnings. The demand for public accountants is set to increase as more companies seek assistance in complying with new accounting standards and regulations. These examples highlight some industry the balance in the prepaid rent account before adjustment at the end of the year is $12000 and represents three months rent paid on december 1 the adjusting entry required on december 31 is accounting practices, but it’s important to note that each sector has its own unique accounting requirements and considerations. Industries such as insurance, telecommunications, hospitality, and retail also have their specific accounting practices tailored to their respective operations and regulations.

Essentially, any information that may be useful to management falls under this umbrella. The definitive exploration of AI and its impact on the accounting profession, according to 595 accounting professionals. In a time of exponential growth, predicting where the world will be in five or ten years is difficult. Many fear the increased prevalence of artificial intelligence, but in reality, the accounting industry needs humanity now more than ever—though in a different capacity. Karbon is an accounting practice management tool with collaboration at its core.