This process allows businesses to input product details such as description, cost, and selling price into QuickBooks, ensuring seamless management of inventory and easy tracking of sales data. By integrating relevant information into the QuickBooks system, businesses can monitor stock levels, set reorder points, and analyze sales patterns, enabling effective financial tracking and management. After this, set up your chart of accounts, which involves creating and categorizing accounts to track your business’s financial transactions. Review the settings and configurations, such as fiscal year, tax form, and preferences, to ensure they align with your business needs. You can create a new company file by copying the existing file with the same vendors, customer contact information, chart of accounts and lists.

QuickBooks Desktop Enterprise Review 2024: Features & Pricing – TechRepublic

QuickBooks Desktop Enterprise Review 2024: Features & Pricing.

My starting file is over 156 MB, after the rebuild it is all of 1.8 MB. It seems that the new version of QB is failing to rebuild data correctly. I need to get an extract to my accountant this weekend…

QuickBooks Pro vs. QuickBooks Premier: What’s the difference?

If you connect a bank or credit card account to one company, it isn’t added or visible from a second. Enter your login information and follow the on-screen prompts to set up the second company. QuickBooks Desktop pricing has changed for 2021, with Intuit turning to a subscription model for its desktop products. You will still be able to purchase the application without a subscription, albeit with a significant increase in price. Both editions offer all of the bookkeeping basics your small business needs, with QuickBooks Premier offering more industry-specific features. These tools enable businesses to make informed decisions and gain a comprehensive understanding of their financial standing.

Users can access system features from the navigation bar to the left of the screen, which also offers access to any add-on features such as time tracking and payroll.

A company file in QuickBooks serves as the financial management hub for a business, housing all the financial data and records necessary for accurate bookkeeping and reporting.

Be wary if someone contacts you claiming to be from Intuit Support but they are not using Glance to remote your machine.

Once the review and verification are completed, it’s essential to back up the company file to protect against potential data loss or corruption.

Integration procedures may include mapping data fields, setting up new accounts, and configuring settings to accommodate the specific requirements of the company.

It begins with the initial decision to set up the company profile, followed by entering basic business information such as the company name, address, and industry type. This foundational stage culminates with the customization of invoices, purchase orders, and other essential forms to reflect the company’s branding and communication style. By configuring key elements such as chart of accounts, business type, tax preferences, and bank account information, users can tailor the software to suit their specific financial management needs. QuickBooks Desktop offers comprehensive features for invoicing, expense tracking, budgeting, and reporting, providing powerful tools for efficient business operations. This vital process allows businesses to store essential information about their customers and vendors, such as names, addresses, phone numbers, email addresses, and payment terms. It enables the accurate recording of transactions, including invoices, bills, and payments for effective financial tracking.

Setting a new company

While you can easily track inventory in QuickBooks Pro, if you sell products on a regular basis it’s best to opt for QuickBooks Premier. One of the biggest differences between QuickBooks Pro and QuickBooks Premier is its inventory management feature. Like QuickBooks Pro, QuickBooks Premier has changed its pricing structure for 2021 and added a subscription option.

There, we’ll walk you through how to customize the style and appearance of your invoices, sales receipts, and estimates to give them a more professional look. Click on the pencil icon or anywhere in the company name section to edit the information. Now how to create a new company in quickbooks desktop that you have your information, log in to your QuickBooks account. From your dashboard, click the cogwheel on the upper right of the screen and choose Account and Settings. If you need anything else about deleting transactions, you can comment below.

QuickBooks Pro vs. QuickBooks Premier: Which Is Right for Your Business?

This process begins by validating the initial setup of the company’s financial information, such as chart of accounts, bank accounts, and tax settings. Once the setup is confirmed, the reconciliation process is crucial to ensure that the data in QuickBooks matches the company’s bank statements and other financial records. This process is crucial for ensuring that all company-specific details, such as sales tax rates, payment terms, and chart of accounts, are accurately inputted and configured. It includes validating the accuracy of initial financial balances, bank account details, and other critical data. I’m glad to further assist you with creating a new file from your existing company file. Before you start a new company file, you’ll need to gather these reports to re-create the accounts receivable and accounts payable year-end balances in the new company file.

This process is crucial for ensuring that all financial transactions are accurately recorded and categorized for easy tracking and reporting. In QuickBooks, users can create, organize, and customize accounts to suit their specific business needs, allowing for clear and efficient management of income, expenses, assets, liabilities, and equity. This customization empowers users to configure the chart of accounts, payment terms, invoice templates, and sales tax rates according to their specific business needs. By adjusting these preferences, companies can streamline their financial operations, improve accuracy in reporting, and ensure that the software reflects their individual processes.

All such information is provided solely for convenience purposes only and all users thereof should be guided accordingly. When you start working with time value of money problems, you need to pay attention to distinguish between present value and future value problems. Another way of looking at this is to say that because of the time value of money, you would take an amount less than $12,000 if you could receive it today, instead of $12,000 in 2years. A ________ is a set amount of pay received by a worker over the course of a year. Any money that you pay out should be represented by a negative number; any money that you receive – by a positive number. If you want to calculate the present value of an annuity , this can be done using the Excel PV function.

The higher the interest rate, the higher the compounded interest earned, all else equal. Finding the present value of an amount of money is finding the amount of money today that is worth the same as an amount of money in the future, given a certain interest rate. Interest, as on a loan or a bank account, that is calculated on the total on the principal plus accumulated unpaid interest. Discount each of these dividends back to the present at a discount rate of 12 percent and then sum them. The discount rate is used by both the creditor and debtor to find the present value of an amount of money.

The information in these materials may change at any time and without notice. I have been using the videos to prepare for the CFA Level II exam. The videos signpost the reading contents, explain the concepts and provide additional context for specific concepts. The fun light-hearted analogies are also a welcome break to some very dry content. I usually watch the videos before going into more in-depth reading and they are a good way to avoid being overwhelmed by the sheer volume of content when you look at the readings. Note that this is the premium payable for an annuity of just $1 per year.

Using the Excel PV Function to Calculate the Present Value of a Single Cash Flow

The discount rate is the sum of the time value and a relevant interest rate that mathematically increases future value in nominal or absolute terms. The word “discount” refers to future value being discounted to present value. The present value of a single amount allows us to determine what the value of a lump sum to be received in the future is worth to us today. It is worth more than today due to the power of compound interest. The present value of a single amount is an investment that will be worth a specific sum in the future. For example, if you invest $1,000 today at an interest rate of 12%, it’ll be worth $2,000 in 5 years.

Future ValueThe Future Value formula is a financial terminology used to calculate cash flow value at a futuristic date compared to the original receipt. The objective of the FV equation is to determine the future value of a prospective investment and whether the returns yield sufficient returns to factor in the time value of money. Just like calculating future values, the present value of a series of unequal cash flows is calculated by summing individual present values of cash flows. In finance, the present value of a series of many unequal cash flows is calculated using software such as a spreadsheet. A comparison of present value with future value best illustrates the principle of the time value of money and the need for charging or paying additional risk-based interest rates.

Paying mortgage points now in exchange for lower mortgage payments later makes sense only if the present value of the future mortgage savings is greater than the mortgage points paid today. As shown above, the future value of an investment can be found by using the present value of a single amount formula and adjusting for compound interest. For example, a timeline is shown below for the example above, where we calculated the future value of $10,000 compounded at 12% for 3 years. For example, suppose you want to know the value today of receiving $15,000 at the end of 5 years if a rate of return of 12% is earned. The value of a future promise to pay or receive a single amount at a specified interest rate is called the present value of a single amount. On 5 February 2012, Anna borrows $80,000 and agrees to repay the loan in 110 days at 9% per annum simple interest.

Everything You Need To Master Financial Modeling

The present time is noted with a “0,” the end of the first period is noted with a “1,” and the end of the second period is noted with a “2.” The Balance uses only high-quality sources, including peer-reviewed studies, to support the facts within our articles. Read our editorial process to learn more about how we fact-check and keep our content accurate, reliable, and trustworthy. Finance Strategists is a leading financial literacy non-profit organization priding itself on providing accurate and reliable financial information to millions of readers each year.

Manulife Financial : Statistical Information Package Updated Template – Marketscreener.com

Manulife Financial : Statistical Information Package Updated Template.

These include white papers, government data, original reporting, and interviews with industry experts. We also reference original research from other reputable publishers where appropriate. You can learn more about the standards we follow in producing accurate, unbiased content in oureditorial policy. Determine the interest rate that you expect to receive between now and the future and plug the rate as a decimal in place of “r” in the denominator. Input the future amount that you expect to receive in the numerator of the formula.

Annuity Due

This example shows that if the $4,540 is invested today at 12% interest per year, compounded annually, it will grow to $8,000 after 5 years. Contractor Jason Barrett bought $8,750 worth of building materials on August 26. The supplier offered a 2.5% cash discount on any amount paid within 7 days. Compute the amount the builder should remit to credit their account for $7,500.

Harold Averkamp has worked as a university accounting instructor, accountant, and consultant for more than 25 years. He is the sole author of all the materials on AccountingCoach.com. A timeline can help us visualize what is known and what needs to be computed.

You don’t earn interest on interest you previously earned.If it is compound interest, you can rearrange the compound interest formula to calculate the present value. Calculating the present value of a single amount is a matter of combining all of the different parts we have already discussed. But first, you must determine whether the type of interest is simple or compound interest.

Ordinary Annuity

The Periods per year cell must not be blank or 0 because this will cause a #DIV/0 error. Also, please note that the returned present value is negative, since it represents a presumed investment, which is an outflow. In other words, if you invested $10,280 at 7% now, you would get $11,000 in a year.

The present value of a single sum tells us how much an amount to be transacted in the future is worth today. If we assume a discount rate of 6.5%, the discounted FCFs can be calculated using the “PV” Excel function. Moreover, the size of the discount applied is contingent on the opportunity cost of capital (i.e. comparison to other investments with similar risk/return profiles). When calculating the present value of annuity, i.e. a series of even cash flows, the key point is to be consistent with rate and nper supplied to a PV formula. To get your answer, you need to calculate the present value of the amount you will receive in the future ($11,000).

The General Formula

Determining the appropriate discount rate is the key to properly valuing future cash flows, whether they be earnings or debt obligations. The present value of annuity can be defined as the current value of a series of future cash flows, given a specific discount rate, or rate of return. For this reason, present value is sometimes called present discounted value.

This is a hypothetical example intended for illustration purposes only. It does not represent the performance of any specific investment or portfolio, nor is it an estimate or guarantee of future performance. Professor James’ videos are excellent for understanding the underlying theories behind financial engineering / financial analysis. The AnalystPrep videos were better than any of the others that I searched through on YouTube for providing a clear explanation of some concepts, such as Portfolio theory, CAPM, and Arbitrage Pricing theory. Watching these cleared up many of the unclarities I had in my head.

Novel scoring system can predict response to 177Lu-PSMA therapy … – Urology Times

Novel scoring system can predict response to 177Lu-PSMA therapy ….

Present value is the current value of a future sum of money or stream of cash flows given a specified rate of return. Present value takes the future value and applies a discount rate or the interest rate that could be earned if invested. Future value tells you what an investment is worth in the future while the present value tells you how much you’d need in today’s dollars to earn a specific amount in the future. Future cash flows are discounted at the discount rate, and the higher the discount rate, the lower the present value of the future cash flows.

The personal accountanted present value is negative, representing an outgoing payment. Broadridge Investor Communication Solutions, Inc. does not provide investment, tax, or legal advice. The information presented here is not specific to any individual’s personal circumstances.

If you happen to be using a program like Excel, the interest is compounded in the PV formula. If it is compound interest, you can rearrange the compound interest formula to calculate the present value. When using a financial calculator, we enter our known values followed by their corresponding function key. Net present value is the difference between the present value of cash inflows and the present value of cash outflows over a period of time. The profitability index is a technique used to measure a proposed project’s costs and benefits by dividing the projected capital inflow by the investment. Investopedia requires writers to use primary sources to support their work.

The formula used to calculate the present value divides the future value of a future cash flow by one plus the discount rate raised to the number of periods, as shown below. Compounded QuarterlyThe compounding quarterly formula depicts the total interest an investor can earn on investment or financial product if the interest is payable quarterly and reinvested in the scheme. It considers the principal amount, quarterly compounded rate of interest and the number of periods for computation.

Present Value of a Perpetuity and Present Values Indexed at Times Other Than t = 0

Economic FactorsEconomic factors are external, environmental factors that influence business performance, such as interest rates, inflation, unemployment, and economic growth, among others. Depending on Mr. A Financial condition, risk capacity decisions can be made. While a conservative investor prefers Option A or B, an aggressive investor will select Option C if he is ready and has the financial capacity to bear the risk. Note that, in line with the general cash flow sign convention, the PV function treats negative values as outflows and positive values as inflows. The annuity due is equivalent to a lump sum of A plus the present value of the ordinary annuity for N-1 years. Series of payments are classified into equal cashflows and unequal cashflows.

Calculate the present value of this sum if the current market interest rate is 12% and the interest is compounded annually. Present value of the money is the value of a particular sum today, it is the current available value of money. The present value is discounted at a certain rate and time to find the future value of the money. Our online tools will provide quick answers to your calculation and conversion needs.

There are some instances where cash flow payments are not equal. The saving pattern of self-employed individuals who save depending on their income level at a particular time is a good case in point. The factor \(\frac – 1 \) is termed as the future value annuity factor that gives the future value of an ordinary annuity of $1 per period. Therefore, we multiply any amount by this factor to get the future value of that particular annuity. Simple Interest Formula Simple interest is when interest is only paid on the amount you originally invested .

In other words, money received in the future is not worth as much as an equal amount received today. In other words, present value shows that money received in the future is not worth as much as an equal amount received today. This means that any interest earned is reinvested and itself will earn interest at the same rate as the principal. In other words, you “earn interest on interest.” The compounding of interest can be very significant when the interest rate and/or the number of years is sizeable. This is equivalent to saying that at a 12% interest rate compounded annually, it does not matter whether you receive $8,511.40 today or $15,000 at the end of 5 years.

This calculator does not take into consideration any federal or state taxes, or any investment fees or expenses.

If you want to calculate the present value of an annuity , this can be done using the Excel PV function.

PV (along with FV, I/Y, N, and PMT) is an important element in the time value of money, which forms the backbone of finance.

The investment will be sold when its future value reaches $5,000.

For this reason, present value is sometimes called present discounted value.

Let’s say you just graduated from college and you’re going to work for a few years, but your dream is to own your own business.

Click enter on your keyboard and you’ll see the value returned is -19,588. Remove the negative symbol in front of it and you get 19,588 or $19,588, as we got with our other formulas. Let’s say you just graduated from college and you’re going to work for a few years, but your dream is to own your own business. You have some money now, but you don’t know how much, if any, you will be able to save before you buy your business in five years.

We’ll discuss PV calculations that solve for the present value, the implicit interest rate, and/or the length of time between the present and future amounts. Bond PricingThe bond pricing formula calculates the present value of the probable future cash flows, which include coupon payments and the par value, which is the redemption amount at maturity. The yield to maturity refers to the rate of interest used to discount future cash flows. Present value of a future single sum of money is the value that is obtained when the future value is discounted at a specific given rate of interest.

Balance of payments Dataset | Released 30 June Quarterly summary of balance of payments accounts including the current account, capital transfers, transactions, and levels of UK external assets and liabilities. Paying interest on capital is a means of rewarding partners for investing funds in the partnership as opposed to alternative investments. As such, it reduces the amount of profit available for sharing in the profit or loss sharing ratio. This means that a debit entry is needed in the appropriation account. The double entry is completed by a credit entry in the current account of the partner to whom the salary is paid. Partners’ salaries

In some ways, the term ‘salaries’ is a misleading description.

We may monitor or record telephone calls to check out your instructions correctly and to help us improve the quality of our service. Calls from abroad are charged according to the telephone service provider’s published tariff. Not all Telephone Banking services are available 24 hours a day, 7 days a week.

What’s the difference between accounts payable and accounts receivable?

The daily arranged overdraft interest rate for using your arranged overdraft, over your interest free amount is based on how you manage any accounts you have with us and on the credit information we hold about you. We will let you know your rate in the pre contract credit information we give you if you apply for an arranged overdraft. Please note that intra-trust trading and recharges may need to be reported within the Counterparty section of the Accounts Return. Counterparty categories are shown against relevant account code on the ‘CoA structures and mappings’ tab within the academies chart of accounts spreadsheet. It is suggested that cost centres should be set up to at least be able to define income and expenditure at Academy level so that completion of the accounts return academy tables, such as benchmarking, can easily be populated.

Illustratethe relevant section of the statement of financial position at year end20X5.

For example, the acquisitions and disposals of foreign shares by UK residents.

Similarly, you should aim to get the most favourable terms from your suppliers.

As a result, our EU to Great Britain import statistics from January 2022 are not directly comparable with previous months.

The current account is made up of the trade in goods and services account, the primary income account and the secondary income account.

The primary purpose of this balance is to calculate overdraft charges. We don’t charge overdraft interest until pending transactions have been settled. All items of income and expense recognised in a period must be included in profit or loss unless a Standard or an Interpretation requires otherwise. [IAS 1.88] Some IFRSs require bookkeeping for startups or permit that some components to be excluded from profit or loss and instead to be included in other comprehensive income. The transaction normally completes in full a day or two later when it will then also be reflected in your ‘Account Balance’. Occasionally you won’t see a debit card payment as a pending transaction.

c. Assets Credit

An operational change implemented by HMRC in January 2022 resulted in a break in the data time series for UK exports to the EU. Although this change does not affect data for March and future months, caution should be taken when interpreting Quarter 1 (Jan to Mar) 2022 data or any periods that include January 2022 data. Balance of payments – revision triangles Dataset | Released 30 June Quarterly summary information on the size and direction of the revisions made to the data covering a five-year period, UK.

If you have £350 in your account and have just paid in a cheque for £50 the Account Balance column will increase to £400 the next day. Once the cheque has cleared, the value of the cheque will be reflected in the balance including pending transactions. The balance sheet codes in the CoA reflect the full range of the DfE’s fixed assets, investments and disposals. You can mark these inactive in your finance system and activate them if you need them in the future. Likewise, if you invest in a new SaaS product, you will need to credit your cash account and debit your asset account accordingly every month, quarter, or year, depending on the payment terms. However, if you needed to finance a new piece of equipment for your business, you would create a debit for your fixed asset account, and credit your liabilities to properly record the debt.

d. transferring journal amounts to ledger accounts.

Ensuring you enter the bank statement balance in Step 2, then repeat steps 1. The reconciling items can be dated on or before the last day of the financial year covered by the previous accounting system). The transactions of Medina Information Service are recorded in the general journal below. You are to

post the journal entries to the accounts in the general ledger.

In line with international standards, the Office for National Statistics’ (ONS’) headline trade statistics contain the UK’s exports and imports of non-monetary gold. This trade can have a large effect on the size of and change in the UK’s headline trade figures. This is because a significant amount of the world’s trade in non-monetary gold takes place on the London markets. Your balance might not be what you were expecting over the weekend and bank holidays. Overdraft Remaining – this shows the remaining amount of your arranged overdraft, this will only be displayed if you are using your limit.

Money worries

It was here that the terms debit and credit (from the Latin debitum and creditum) were first employed. If you sell £1,000 worth of T-shirts, you’ve gained £1,000 in your cash account. As such, you would offset this debit to your cash account by crediting your inventory or asset account by £1,000.

A contribution will be a credit entry in the capital account and a debit entry in the bank account, and a withdrawal will be a debit entry in the capital account and a credit entry in the bank account. If goodwill is to be retained in the partnership and therefore continue to be recognised as an asset in the partnership accounts, then no further entries are required. A partner’s total capital is the sum of the balances on their capital account and their current account. Share of residual profit

This is the amount of profit available to be shared between the partners in the profit or loss sharing ratio, after all other appropriations have been made. The profit or loss sharing ratio is sometimes simply called the ‘profit sharing ratio’ or ‘PSR’.

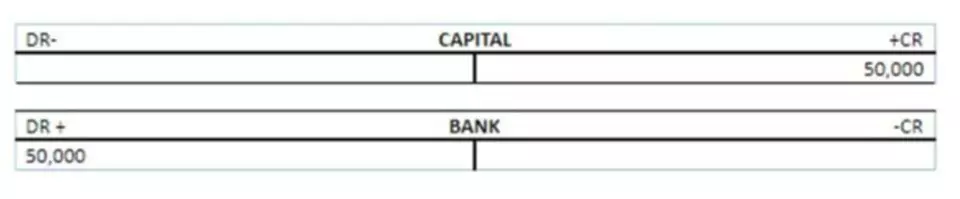

Example of a capital account

This ensures expenditure is allocated to the correct field in the DfE’s financial returns. The accounting treatment for Salix loans is the same as for other loans, except that repayments need to gross back up the GAG rebatement. The draft financial statement spreadsheet can be automatically populated from the trusts general ledger if they are able to take advantage of the API functionality. Alternatively, a spreadsheet which can be manually populated will be available on the CoA and automation webpage in due course. This is because the trust level data is reported in the SoFA, but is requested at central services and academy level in the benchmarking tables, although again, the overall total for the trust must equal zero. •Using the PIN transaction, select the foreign supplier from the Supplier Accounts list and select the foreign currency from the Currency drop-down.

What is normal balance of accounts debit and credit?

Normal Balance of an Account

As assets and expenses increase on the debit side, their normal balance is a debit. Dividends paid to shareholders also have a normal balance that is a debit entry. Since liabilities, equity (such as common stock), and revenues increase with a credit, their “normal” balance is a credit.

You can use a current account to pay regular bills, by setting up Direct Debits and standing orders. There are only extremely rare circumstances where depreciation should be charged on land specifically, which is why there is no specific chart of accounts code for depreciation against freehold and leasehold land. The current chart of accounts mapping to the ‘Academies accounts return’ is shown in column G.

Desktop has an Enterprise plan for $1,340 per year and allows up to 40 users. No matter the Desktop plan you choose, you can install your software on multiple computers—up to however many users your plan allows. If you’re like most users, you have an average of two to three finance apps on your smartphone.

QuickBooks is an accounting software program that offers a variety of features to help small businesses manage their finances.

Zoho Invoice is a well-known small business online invoicing software that is easy to use.

On September 4, 2020, Intuit rolled out QuickBooks 2021 with improved payment process and automated features.

Personal expenses aren’t recognized as business expenses and these can’t technically be deducted from your business’ accounts.

Not only are there different tiers of features depending on the size of your business, but there are also desktop and online versions for most products. They can also be customized through add-ons to get the features you are looking for. Using QuickBooks for personal use is actually not a bad idea as this software is equipped with all the facilities that are required for the management of finances. With the help of QuickBooks software, you can easily manage all your day-to-day spending that too at one place, track your expenses on the purchases you are doing, and can pay people on time.

Products

Quite often, you are not the only person in your company who needs to know how to use QuickBooks or QuickBooks Online. It doesn’t make financial sense to sign each employee up for an online course or make them read a book. And you certainly don’t want them to come to you with quickbooks self employed every question . Whether you need to train your assistant or a staff accountant, it’s much easier to accomplish when you hire a trainer. You can have them trained in the same setting as you or separately—the most important part is that you won’t have to do it personally.

Now that you know everything about the Tips for Using QuickBooks for Your Personal Finances, you can get a greater understanding of your financial position. However, if you still are stuck or have any queries you can reach out to the Dancing Numbers team for quick and easy assistance. In your bank register, change the display options to check the cleared items.

How to Enter Cash Expenses in Quicken

The difference between Quicken vs QuickBooks is that Quicken is primarily for managing personal finances, whereas QuickBooks is a double-entry bookkeeping system for small businesses. However, Quicken does have features to track income and expenses of rental houses and simple one-person businesses.

Retroactive reporting of all major general governmental infrastructure assets is encouraged at that date. Phase 3 governments are encouraged to report infrastructure retroactively, but may elect to report general infrastructure prospectively only. The net assets of a government should be reported in three categories—invested in capital assets net of related debt, restricted, and unrestricted. Permanent endowments or permanent fund principal amounts included in restricted net assets should be displayed in two additional components—expendable and nonexpendable. These liabilities become contingent whenever their payment contains a reasonable degree of uncertainty. Only the contingent liabilities that are the most probable can be recognized as a liability on financial statements.

Many citizens—regardless of their profession—participate in the process of establishing the original annual operating budgets of state and local governments. Governments will be required to continue to provide budgetary comparison information in their annual reports. An important change, however, is the requirement to add the government’s original budget to that comparison. Many governments revise their original budgets over the course of the year for a variety of reasons. Requiring governments to report their original budget in addition to their revised budget adds a new analytical dimension and increases the usefulness of the budgetary comparison. However, we believe that the information will be important—in the interest of accountability—to those who are aware of, and perhaps made decisions based on, the original budget.

Summary of Statement No. 34

These materials were downloaded from PwC’s Viewpoint (viewpoint.pwc.com) under license. If some amount within the range of loss appears at the time to be a better estimate than any other amount within the range, that amount shall be accrued. When no amount within the range is a better estimate than any other amount, however, the minimum amount in the range should be accrued.

Financial managers also will be in a better position to provide this analysis because for the first time the annual report will also include new government-wide financial statements, prepared using accrual accounting for all of the government’s activities. It measures not just current assets and liabilities but also long-term assets and liabilities (such as capital assets, including infrastructure, and general obligation debt). It also reports all revenues and all costs of providing services each year, not just those received or paid in the current year or soon after year-end. To report additional and detailed information about the primary government, separate fund financial statements should be presented for governmental and proprietary funds.

Free Accounting Courses

The rule applies more to biotech and drug companies who conduct trials and testing phases, which may not be as relevant to investors besides the impact of the finished product itself. FASB Interpretations are published by the Financial Accounting Standards Board (FASB). They extend or explain existing standards (primarily published in Statements of Financial Accounting Standards). Professionals undergo years of education in order to truly understand the already existing principles and accounting standards. However, FASB makes sure to continually educate and update the knowledge and expertise of its accountants and other professionals to uphold its mission and purpose while also enabling transparency. Banks that issue standby letters of credit or similar obligations carry contingent liabilities.

To report additional and detailed information about the primary government, separate fund financial statements should be presented for governmental and proprietary funds.

To allow users to assess the relationship between fund and government-wide financial statements, governments should present a summary reconciliation to the government-wide financial statements at the bottom of the fund financial statements or in an accompanying schedule.

Fund statements also will continue to measure and report the “operating results” of many funds by measuring cash on hand and other assets that can easily be converted to cash.

The FASB’s mission, advertised strongly on their website, is to continuously update and enable accountants to work with better accounting principles.

The Camden, Maine, bank found the switch from an Excel-based model saves time and gives it more confidence in the accuracy of its allowance.

The Securities and Exchange Commission (SEC) designated the FASB as the organization responsible for setting accounting standards for public companies in the U.S.

On the other hand, when governments charge a fee to users for services—as is done for most water or electric utilities—fund information will continue to be based on accrual accounting (discussed below) so that all costs of providing services are measured. If a contingent liability is deemed probable, it must be directly reported in the financial statements. Nevertheless, generally accepted accounting principles, or GAAP, only require contingencies to be recorded as unspecified expenses.

List of FASB Interpretations

Following a consistent set of standards enables a more efficient market and economy. PwC refers to the US member firm or one of its subsidiaries or affiliates, and may sometimes refer to the PwC network. This content is for general information purposes only, and should not be used as a substitute for consultation with professional advisors. FASB Statement of Financial Accounting Standards No. 5 requires any obscure, confusing or misleading contingent liabilities to be disclosed until the offending quality is no longer present. Future costs are expensed first, and then a liability account is credited based on the nature of the liability. In the event the liability is realized, the actual expense is credited from cash and the original liability account is similarly debited.

What is the FAS 5 reserve standard?

FAS 5 prescribes standards for reserving for loss contin- gencies only. Gain contingencies, which were previously ad- dressed in Accounting Research Bulletin No. 50 (Oct. 1958), generally may not be reflected as assets in an entity's financial statements.

Internal service funds also should be reported in the aggregate in a separate column on the proprietary fund statements. MD&A should provide an objective and easily readable analysis of the government’s financial activities based on currently known facts, decisions, or conditions. MD&A should include comparisons of the current year to the prior year based on the government-wide information. It should provide an analysis of the government’s overall financial position and results of operations to assist users in assessing whether that financial position has improved or deteriorated as a result of the year’s activities. In addition, it should provide an analysis of significant changes that occur in funds and significant budget variances.

Governments with less than $10 million in revenues (phase 3) should apply this Statement for periods beginning after June 15, 2003. Governments that elect early implementation of this Statement for periods beginning before June 15, 2000, should also implement GASB Statement No. 33, Accounting and Financial Reporting for Nonexchange Transactions, at the same time. If a primary government chooses early implementation of this Statement, all of its component units also should implement this standard early https://accounting-services.net/what-is-fas-5/ to provide the financial information required for the government-wide financial statements. Proprietary fund statements of revenues, expenses, and changes in fund net assets should distinguish between operating and nonoperating revenues and expenses. These statements should also report capital contributions, contributions to permanent and term endowments, special and extraordinary items, and transfers separately at the bottom of the statement to arrive at the all-inclusive change in fund net assets.

Under GAAP, the listed amount must be “fair and reasonable” to avoid misleading investors, lenders, or regulators. Estimating the costs of litigation or any liabilities resulting from legal action should be carefully noted. The GASB expresses its thanks to the thousands of preparers, auditors, academics, and users of governmental financial statements who have participated during the past decade in the research, consideration, and deliberations that have preceded the publication of this Statement. We especially appreciate the input of those who participated by becoming members of our various task forces, which began work on this and related projects as early as 1985.

Please Sign in to set this content as a favorite.

Separate fiduciary fund statements (including component units that are fiduciary in nature) also should be presented as part of the fund financial statements. Fiduciary funds should be used to report assets that are held in a trustee or agency capacity for others and that cannot be used to support the government’s own programs. Required fiduciary fund statements are a statement of fiduciary net assets and a statement of changes in fiduciary net assets. We have an open decision-making process that encourages broad public participation. To demonstrate whether resources were obtained and used in accordance with the government’s legally adopted budget, RSI should include budgetary comparison schedules for the general fund and for each major special revenue fund that has a legally adopted annual budget.

Appendix D summarizes how the new standards would be incorporated into the GASB’s June 30, 1999, Codification of Governmental Accounting and Financial Reporting Standards.

The FASB plays a pivotal part in the functioning of several regulatory bodies in the U.S., as accounting standards are important for an efficient market.

The requirements of this Statement are effective in three phases based on a government’s total annual revenues in the first fiscal year ending after June 15, 1999.

Professionals undergo years of education in order to truly understand the already existing principles and accounting standards.

Governments will be required to continue to provide budgetary comparison information in their annual reports.

For the first time, those financial managers will be asked to share their insights in a required management’s discussion and analysis (referred to as MD&A) by giving readers an objective and easily readable analysis of the government’s financial performance for the year. This analysis should provide users with the information they need to help them assess whether the government’s financial position has improved or deteriorated as a result of the year’s operations. The detailed authoritative standards established by this Statement are presented in paragraphs 3 through 166.